When oil prices sneeze, risk assets catch pneumonia. Crypto is currently reaching for the tissues.

Prediction market Polymarket now shows a record 73% probability that US oil prices will breach $90 per barrel this month — a level not seen since October 2023. Bitcoin responded by slipping below $71K, while the broader crypto Fear & Greed Index sits at a grim 18, deep in “Extreme Fear” territory.

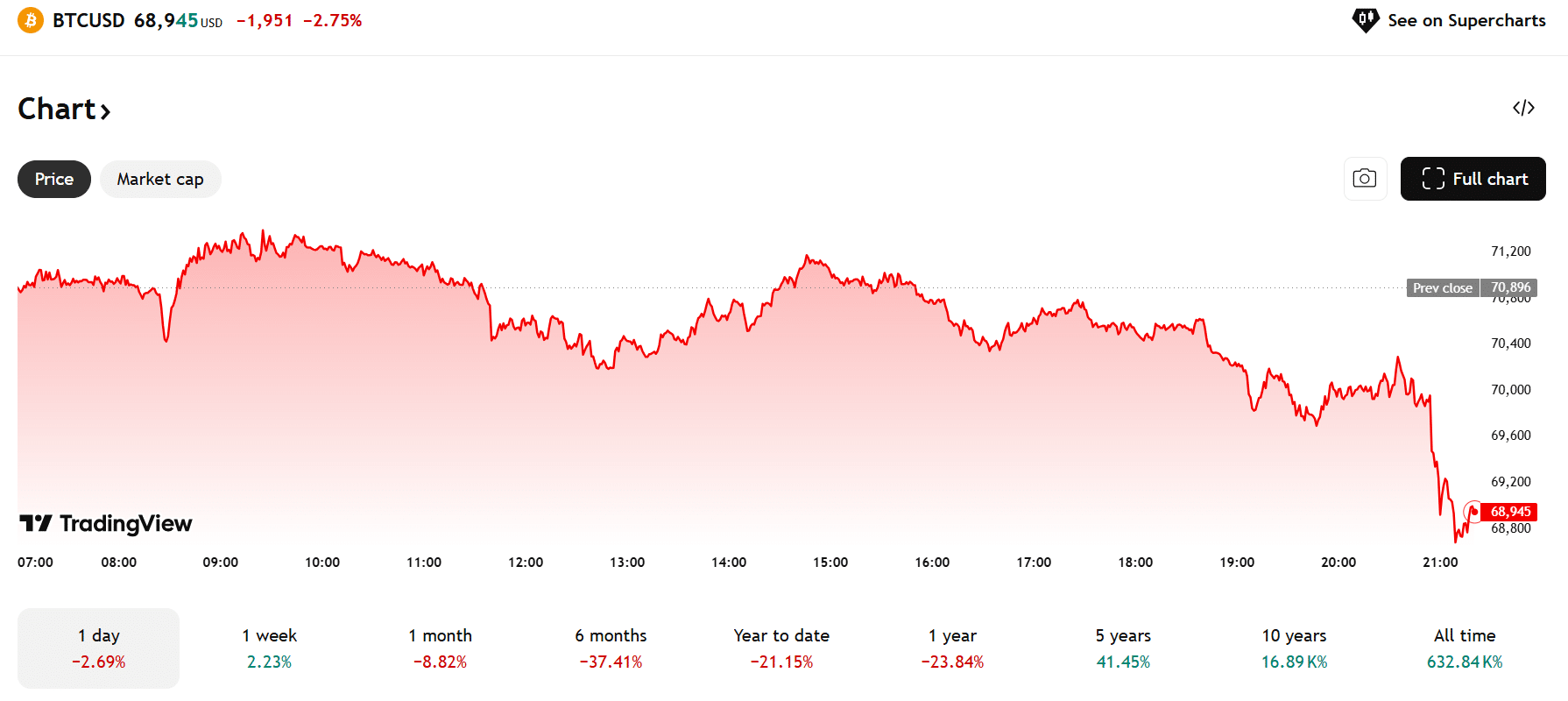

The numbers tell a painful story

Bitcoin dropped 2.6% over the past 24 hours, trading below the $71K mark that bulls had been defending. The weekly picture is slightly less bleak — BTC is still up 4.3% over seven days — but the daily momentum clearly belongs to the sellers.

Ethereum fared no better, shedding 2.5% to drift near $2,075. That’s a psychologically important zone for ETH holders who remember the asset comfortably sitting above $3,000 not long ago.

Solana took the hardest hit among major assets, falling 3.0% to slide toward $88. XRP settled around $1.40, joining the broader retreat without much fanfare.

The Fear & Greed Index reading of 18 is worth sitting with for a moment. Last week it was 13 — also “Extreme Fear.” So technically, sentiment has improved. Going from “apocalyptic dread” to merely “extreme dread” isn’t exactly a victory lap, but it’s something.

Why oil matters for your crypto portfolio

The connection between crude oil and digital assets might not seem obvious at first glance. Bitcoin doesn’t run on diesel. Ethereum validators don’t need gasoline. But the relationship is real and runs through a pretty straightforward chain of logic.

Rising oil prices feed directly into inflation expectations. When energy costs climb, everything from shipping to manufacturing gets more expensive. That cost pressure flows through to consumer prices, which is precisely what the Federal Reserve watches when deciding interest rate policy.

In English: expensive oil makes the Fed less likely to cut rates, and crypto loves rate cuts.

The $90-per-barrel threshold is particularly significant because it represents a psychological barrier the market hasn’t tested in roughly 18 months. If Polymarket’s 73% probability proves correct, it would signal a meaningful shift in the energy landscape that could ripple through every corner of financial markets.

Higher energy costs also directly impact Bitcoin mining operations, squeezing margins for an industry already navigating post-halving economics. When it costs more to run the machines that secure the network, miners face uncomfortable choices — absorb the losses, sell more Bitcoin to cover costs, or shut down unprofitable rigs. None of those options are particularly bullish.

The macro backdrop extends beyond just oil. Global trade tensions remain elevated, and several major economies are showing signs of slowing growth. When institutional investors get nervous about the broader economic picture, they tend to reduce exposure to volatile assets first. Crypto, for better or worse, still sits squarely in that category for most traditional portfolio managers.

What investors should watch from here

The extreme fear reading is a double-edged sword, and experienced market participants know it. Historically, periods of maximum pessimism in the Fear & Greed Index have often preceded significant rallies. The classic Warren Buffett playbook of being greedy when others are fearful has worked in crypto markets multiple times — but it requires genuine conviction and an iron stomach.

That said, there’s an important distinction between fear driven by sentiment and fear driven by structural macro forces. The current anxiety has real economic fundamentals behind it. Oil prices don’t care about crypto Twitter’s mood. If energy costs genuinely surge past $90 and stay there, the pressure on risk assets could persist well beyond a typical sentiment-driven dip.

One bright spot buried in the data: the Morpho Ecosystem category surged 63.9% over the past week, according to CoinGecko. It’s a reminder that even in broad market downturns, specific narratives and niches can dramatically outperform. Investors who focus exclusively on BTC and ETH price action might miss rotations happening beneath the surface.

The key variable to monitor is whether oil actually breaches and holds above $90. Prediction markets are useful gauges of consensus expectations, but they’re not crystal balls. If oil stalls below that level, the fear premium currently baked into crypto prices could unwind quickly. If it blows through $90 and heads toward $95 or $100, expect the current drawdown to deepen.

Bitcoin’s ability to hold the $70K level will be the most important technical signal in coming days. A decisive break below that round number could trigger a cascade of liquidations and stop-losses that accelerate selling pressure. Conversely, a strong bounce from current levels would suggest buyers view this as a macro-driven dip worth buying.

Ethereum’s positioning near $2,075 puts it in a similarly precarious spot. The $2,000 level has served as significant support multiple times, and a test of that zone feels increasingly likely if the macro picture doesn’t improve.

For Solana, the decline toward $88 comes after a period of relative strength in its ecosystem metrics. Network activity and developer engagement have remained solid, which creates an interesting divergence between on-chain fundamentals and price action. That kind of disconnect tends to resolve — the question is which direction.

Bottom line: Crypto markets are caught in a macro vice grip where rising oil prices, stubborn inflation fears, and extreme sentiment readings converge to create genuine uncertainty. The Fear & Greed Index at 18 suggests plenty of pain is already priced in, but with Polymarket’s oil call at record conviction levels, the external pressure may not be done yet. Sometimes the smartest move in extreme fear is patience — not panic, but not premature heroism either.

Disclosure: This article was edited by Estefano Gomez. For more information on how we create and review content, see our

Editorial Policy.