Wall Street was bracing for a gut punch. It got a pleasant surprise instead.

April’s nonfarm payrolls landed at 115K new jobs, nearly double the 55K that economists had penciled in. In a market climate defined by tariff anxiety and rising fuel costs, “not as bad as feared” was more than enough to spark a Friday rally across both equities and digital assets.

The numbers that matter

The headline figure tells most of the story. 115K jobs added in April versus consensus expectations of 55K. That’s not a blockbuster number by historical standards, but context is everything. Markets had spent the week pricing in a potential disaster scenario, and the actual data came in looking downright healthy by comparison.

Unemployment held steady at 4.3%, a figure that would have seemed unremarkable six months ago but now carries extra weight. Tariff headwinds and soaring fuel costs had economists worried about cracks forming in the labor market. Those cracks didn’t show up, at least not yet.

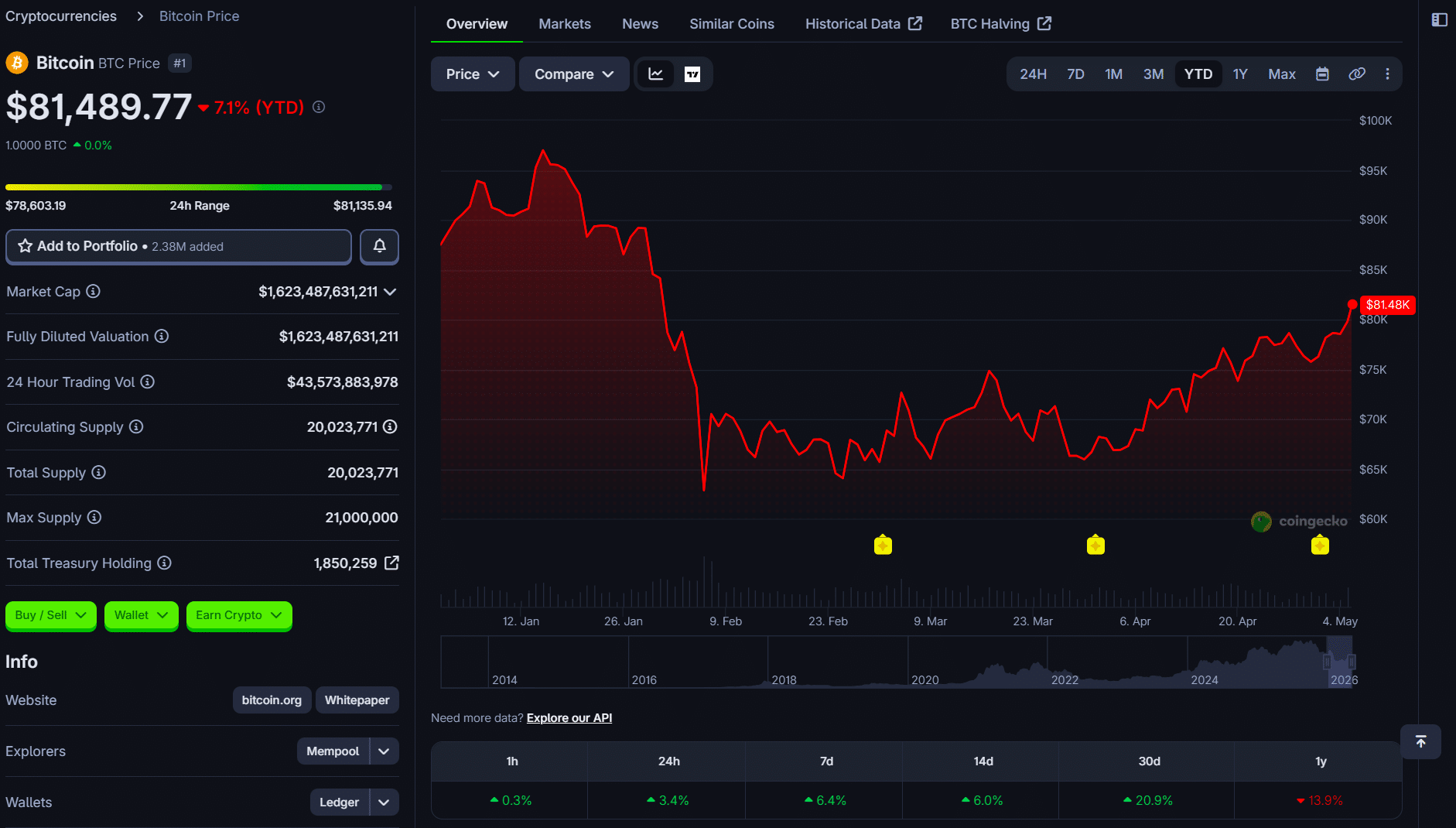

The reaction across crypto was measured but positive. Bitcoin held near $80K, down a modest 0.3% over 24 hours but up 2.1% on the week. Ethereum traded around $2,300, slipping 0.8% on the day. Solana edged toward $89 with a 0.7% daily gain, and XRP sat at $1.39.

Nobody’s popping champagne. But nobody’s panic-selling either.

Why crypto cares about jobs data

Here’s the thing about nonfarm payrolls: they’re a lagging indicator dressed up as a leading one. The jobs number tells you where the economy was, not where it’s going. But markets trade on narrative, and the narrative shifted Friday morning from “the economy is falling apart” to “the economy is bending but not breaking.”

That distinction matters for crypto in a very specific way. A weak jobs number would have amplified calls for emergency Fed rate cuts, which sounds bullish for risk assets until you realize that emergency cuts signal panic. Markets don’t want the Fed cutting rates because the patient is coding. They want the Fed cutting rates because inflation is cooling and the economy is stable enough to handle looser policy.

A 115K print threads that needle. It’s soft enough to keep rate-cut expectations alive but strong enough to avoid triggering recession alarms. Think of it as the Goldilocks porridge of labor market data: not too hot, not too cold, just lukewarm enough to keep everyone calm.

The Crypto Fear and Greed Index, tracked by Alternative.me, sat at 38 on Friday, firmly in “Fear” territory. That’s still cautious, but it marks a notable improvement from 26 just a week ago. The index essentially doubled its distance from “Extreme Fear” in seven days, and the jobs data likely contributed to that shift in sentiment.

For perspective, a reading of 38 means the market is nervous but functional. A reading of 26 means the market is hiding under the bed. The move from one to the other in a single week suggests that bearish positioning was getting crowded and that traders were looking for any excuse to cover shorts and re-enter risk.

The bigger picture for investors

Look, one jobs report doesn’t change the macro landscape. Tariffs are still creating uncertainty for businesses trying to plan ahead. Fuel costs are still elevated, squeezing margins for consumers and companies alike. The labor market being “fine for now” doesn’t mean it’ll be fine in three months.

But positioning matters, and heading into the weekend, crypto markets are sitting in a notably different spot than they were a week ago. Bitcoin’s 2.1% weekly gain might not sound like much, but it came against a backdrop of persistent fear and macro headwinds. Holding $80K as a floor rather than testing it as a ceiling is a meaningful shift in market structure.

The DeFi sector, according to CoinGecko data, was flat on the week, coming in at 0.0% for seven-day performance. That’s actually the top-performing category, which tells you something about how defensive the broader market remains. When “didn’t lose money” counts as winning, you know sentiment still has room to recover.

What investors should watch next is whether the jobs data changes the Fed’s calculus at all. The unemployment rate holding at 4.3% gives the central bank cover to stay patient, which means the “higher for longer” rate environment probably isn’t going anywhere soon. For crypto, that means the next leg higher likely needs a catalyst beyond macro relief, whether that’s ETF flow data, on-chain activity picking up, or a genuine shift in monetary policy expectations.

The jobs report bought the market some time. What it does with that time is the real question.

Disclosure: This article was edited by Estefano Gomez. For more information on how we create and review content, see our

Editorial Policy.